The VAT is a tax payable by companies in the Netherlands, whether they are resident businesses or foreign entrepreneurs.

Almost every company is subject to this tax and it applies to the sales price of the products and/or services they offer to clients.

Our tax lawyers in Netherlands highlight the main requirements for VAT registration, the different approaches according to tax residency, as well as other aspects concerning this type of tax.

For complete information about the current tax laws and reporting requirements, please reach out to our team.

| Quick Facts | |

|---|---|

| We offer VAT registration services |

Yes |

|

Standard rate |

21% |

|

Lower rates |

0%, 9% |

| Who needs VAT registration | All VAT payers (all those engaging in VAT-taxable activities) |

| Time frame for registration | Approximately 10 days |

| VAT for real estate transactions |

Property sale and letting exempted from VAT in certain cases |

| Exemptions available |

Education, childcare and healthcare services |

| Period for filing | Within 1 month after the report period |

| VAT returns support | Yes, upon request |

| VAT refund | Only in some cases for goods or services used for business purposes |

| Local tax agent required | Recommended |

| Who collects the VAT | The Dutch Tax and Customs Administration |

| Documents for VAT registration | The Dutch Tax and Customs Administration receives the details for registration from the Netherlands Chamber of Commerce once the company is entered into the Dutch Business Register |

| VAT number format | NL + 9 digits + B + 2 check digits |

| VAT de-registration situations | When the company is deregistered from the Chamber of Commerce |

| Voluntary registration availability (YES/NO) | NO, VAT registration in Netherlands is mandatory. |

|

VAT registration for sole traders |

Mandatory, but you can apply for the small businesses scheme (KOR) if your annual turnover is below 20,000 euros, and be VAT exempt. |

|

VAT registration for branches |

Mandatory, but some exceptions may apply. Our Dutch lawyers can offer more details. |

| VAT registration for liaison offices (YES/NO) |

NO |

| VAT for e-commerce activities |

Mandatory, as per the European Union taxation scheme. |

| Threshold for e-commerce VAT registration |

More than 10.000 euros/ year |

| Record-keeping requirements |

7 years |

| Invoice must contain VAT rate (YES/NO) |

YES |

| Other invoice requirements |

– VAT identification number, – invoice date, – invoice number, – business name and address, – customer name and address, – supplied goods/services and quantity, – Dutch Business Register number (if applied), – date of supply |

| Simplified invoices | If the total amount of the invoice does not exceed 100 euros. |

| Invoice issue expiration date |

Generally 5 years, but there is a 2 years exception for some invoices. Our attorneys can detail. |

| Penalties for late VAT returns |

3% of the unpaid, partially unpaid, or not paid on-time tax |

| VAT number for EORI registration |

A VAT number is mandatory before applying for the EORI number. |

| Annual VAT return |

Not required |

| Reverse charge mechanism | Makes the recipient responsible for paying VAT on certain transactions involving non-established businesses. |

Table of Contents

Dutch VAT Registration for a foreign company

Whenever foreign investors provide goods and services in the country, their activities are also covered by the VAT laws in the country.

Foreign investors must not only calculate and pay the tax but also make the necessary report submissions. In some cases, a VAT deduction claim can be made.

A foreign entrepreneur involved with Dutch VAT may need to register for VAT purposes, with the Tax and Customs Administration.

A special registration form is in place, which can be sent to the address of the tax authorities.

Foreign entrepreneurs who require assistance during this step can rely on the services provided by our team of experts.

A foreign company must register for VAT in the Netherlands in the following cases:

- it imports or exports goods and is required to submit a VAT return (intra-Community goods or services);

- the company is from a non-EU country and is not required to submit a VAT return but it does with to claim a VAT refund;

- the company is a non-EU one that wishes to use the One Stop Shop in the Netherlands.

VAT registration for foreign companies may not always be compulsory. It is not always necessary to register if the foreign company falls under one of the following categories:

- the company is a non-EU one that does not file a VAT return;

- the company is based outside of the European Union;

- the company supplies goods in the EU to customers who do not need to submit VAT returns (for example, private individuals);

- the company is registered for the Union Scheme in another EU country;

- the company supplies goods using a digital platform and the customers are private individuals who are not required to submit a VAT return in the Netherlands;

- the company is registered for the non-Union scheme in another EU country, other than the Netherlands.

Although not mandatory, a foreign company can use a tax representative. when this is the case, the representative will be the one to deal with all of the existing VAT issues.

Foreign companies doing business in the Netherlands that do not have a VAT representative will need to handle the matters with the corresponding tax office. For foreign entrepreneurs, this is the Tax and Customs Department of International Issues.

Foreign companies operating in the Netherlands should also be aware of the manner in which they can access VAT refunds.

These refunds may be claimed when the applicant complies with a set of conditions. Among these, our attorneys in the Netherlands list the following: the use of the goods and services was for business and not personal purposes and the use of the said goods and services was for activities that are subject to VAT application.

The claim refund will only be taken into consideration when the applicant is not required to file a Dutch tax return, the VAT has been charged to the applicant and the VAT is deductible as an input tax for the applicant. The claimed amount must be at least 50 euros per calendar year (other minimum amounts can apply). For businesses in the food and drink catering sector, the VAT cannot be deducted.

When a business supplied goods and services in the Netherlands and it is not subject to the Dutch VAT, the VAT rate will usually be reverse-charged to the client.

This is the case when the client is another business with a permanent establishment in the Netherlands or when it is a company (legal entity) that has been established in the country as per the usual company registration laws.

When a foreign entrepreneur with goods in a Dutch city supplies these said goods to a client with an establishment or permanent establishment in the Netherlands, the foreign entrepreneur will issue an invoice that will include the fact that VAT has been reverse charged in that case.

Our team of Dutch lawyers can provide foreign investors in the Netherlands with more information on reverse charging on services and goods.

In some situations, taxpayers can object to a decision made by the Tax and Customs Administration. One of our lawyers in the Netherlands can help those who are confronted with this submit a letter of objection (within the six-week period).

The decision issued by the Administration can be appealed. One of our lawyers can help you with more information about objecting to these decisions.

As previously mentioned, foreign investors in the Netherlands may appoint a tax representative who will handle the requirements set forth by the Tax and Customs Administration.

Working with a tax representative is mandatory when the entrepreneur wishes to use the reverse charge mechanism on import.

Having a representative does not mean that the business owner is not liable for tax purposes. The main requirements for a tax representative are that he must be based in the country and he must offer financial security for the VAT. His main duties are filling in the VAT return, filling in the intra-community transactions statement, and applying the reverse-charge mechanism on imports.

VAT registration for a local company

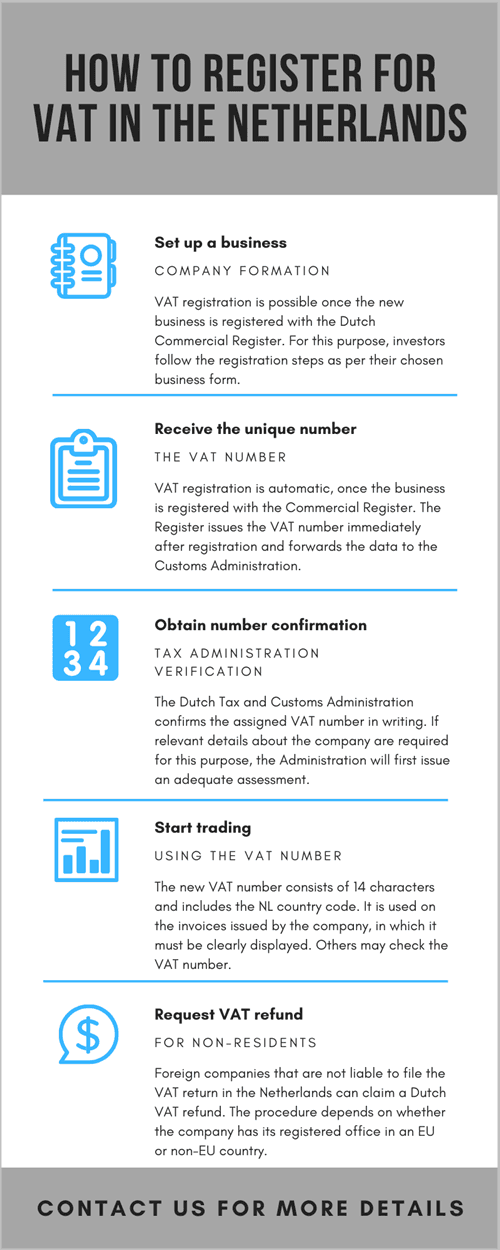

Once the Dutch company is subscribed to the Trade Register, the Commercial Chamber automatically transfers the company information to the tax authorities.

At the same time, your company is subject to VAT registration in Netherlands. The VAT number in the Netherlands is issued immediately upon registration with the Chamber of Commerce for sole proprietorship and within five working days for other forms of business: partnership, limited liability company, corporation and other.

Once you registered for VAT in the Netherlands and received the VAT number, there is some information about this tax number you need to know: the VAT number consists of 14 characters: the country code NL, followed by the Partnerships Legal Information Number (RSIN) or the Citizen Service Number (BSN), plus a 3 digit code between B01 and B99.

As you are registered for VAT in the Netherlands, the tax authorities mention the company’s VAT number on the letters and forms receive. In some forms, the tax authorities use the tax number, which is almost the same as the VAT number, but it has no country code.

After the registration with the Trade Register, the CoC number is issued and, as a legal entity or joint venture, there will also be issued a number of Entities and Collaboration Information (RSIN). Moreover, each branch of the company will receive a unique establishment number of 12 digits.

One of our tax lawyers can provide investors with more information about VAT registration in Netherlands in 2024.

How long does it take to obtain a Dutch VAT number?

The registration for VAT in the Netherlands takes approximately 5 days. It should be noted that companies interested in carrying out trading activities outside the Netherlands will be required to apply for an EORI number with the Tax Administration and Customs Office.

Facts about the VAT registration procedure in the Netherlands

A company in the Netherlands is required to register with the Commercial Register of the Chamber of Commerce (CoC), in order to appear as a VAT payer in the Netherlands, as well as for other fiscal duties. This applies to any type of legal entity such as a private limited company, limited liability company, association, or foundation.

Registration with the CoC is also required for a partnership (such as a general partnership) and for a sole proprietorship. For registration with the Commercial Register, there must be paid a one-time registration fee in the amount of EUR 50.

Some important facts about VAT registration in the Netherlands are highlighted below by our team of Dutch lawyers:

- eligibility: the Dutch Tax and Customs Administration makes a special assessment for VAT eligibility; entrepreneurs may be liable for VAT purposes and not the income tax;

- usage: the VAT number issues once the Dutch Commercial Register completes the registration procedure will be indicated on all of the issues invoices.

- calculation: the VAT is calculated on the price and costs of the provided goods and services.

- exemption: some goods and services in the Netherlands are exempt from VAT, examples including services for childcare.

Dutch VAT invoicing requirements

Foreign and local citizens and companies applying for a VAT number with the Dutch authorities will have the obligation of displaying this number on each invoice they issue. They are also required to file VAT reports with the local tax office. All invoices must contain specific information about the VAT, among which:

- the client’s VAT number;

- the seller’s VAT identification number;

- a description of the goods/services sold;

- the net amount subject to VAT;

- the VAT rate;

- the amount due as a VAT;

- the amount with the VAT included.

It is also important to notice that upon company dissolution, a Dutch business will also be de-registered with the tax office and its VAT number will be deleted. A notification will be issued by the tax authorities in this sense.

Claiming the VAT refund in the Netherlands

Companies that purchased goods as per their business purposes or that incurred other business-specific costs can claim a VAT refund. This process differs based on whether or not the business is based in an EU or a non-EU country (as seen above, non-resident companies can apply for these refunds).

Below, our lawyers who specialize in VAT registration in the Netherlands describe the two situations, based on where the company is incorporated.

When the company is established in an EU country, a VAT refund may be claimed over the past five years.

This request is made in a digital form to the tax authorities in the EU country in which the company is based. The submission deadline is October 1st in most countries in the European Union. However, we recommend verifying this date as the VAT request is no longer valid after this date.

When an entrepreneur submits the refund request, the tax authorities in the country where it was submitted forward it to the Dutch Tax Department. In turn, the Department forwards the confirmation of receipt to the email address provided by the entrepreneur.

In most cases, the decision for the refund is communicated within four months from the submission date. In some cases, this may differ. When the answer is a positive one (meaning that the refund was approved), the Dutch Tax Department is to pay the amount within ten days. When more information is required for the assessment of the applications (for example, not all of the documents are submitted with the initial application), this period may differ and in turn, the payment may be postponed.

When the business is incorporated in a non-EU country, the business owner needs to fill in a special form for the registration of foreign business aid.

This step also includes a questionnaire that determines if the application may be filed immediately or if the business also needs to apply for a VAT number in the Netherlands or a registration number.

When filing a VAT refund request, the business must also include the following documents: an entrepreneurship statement from the tax administration in the country of origin, the original invoices as well as relevant import documents.

Companies in a non-EU country, for example, the United States, can submit a VAT refund request for up to five years after e year in which the business was charged for VAT purposes. However, entrepreneurs should be aware that when they claim the return for the years 2013-2016 they do not have the right to appeal to the courts against the decision issued by the Dutch tax authorities. One of our lawyers can provide more details.

Entrepreneurs who are interested in finding out more information about VAT returns and how they can make the refund calculation, as well as other calculations, can reach out to our tax lawyers in the Netherlands. We can also provide more details about the VAT number in the Netherlands, in addition to the details already mentioned in this article.

We invite you to watch a short video on VAT registration in the Netherlands:

What are the VAT rates in the Netherlands in 2024?

The Tax and Customs Administration in the Netherlands imposes different value-added tax rates, according to the types of services. these are the following:

- 21%: this is the general tariff applicable to most of the services provided by Dutch companies.

- 9%: this low tariff applies to food and drinks, agricultural products and services, medicines, daily newspapers, magazines and other common products and services,

- 0%: this mainly to the supply of goods from the Netherlands to another country in the EU; it also applies to the international transport of passengers.

In some industries and for certain activities, you are exempt from VAT and you will not charge this tax, for example, collective interests, composers, writers, cartoonists and journalists, financial and insurance services, fund-raising activities, healthcare, gambling, childcare, education, radio and television, sports organizations and sports clubs.

An agricultural scheme applies to market gardeners, livestock farmers as well as foresters in the Netherlands. The goods and services supplied by business owners in these fields is also subject to the VAT exemption.

One of our Dutch lawyers can provide more details about this regime and, in general, about the goods, services, and professions that are subject to the VAT exemption. In case you need accounting services in another country, for example in Malta, you can contact our partners.

Digital services are subject to different VAT rules, meaning that they are taxed in the country of the client (where he lives or where he is established). These types of services refer to telecommunication, broadcasting and electronic services. One of our lawyers in the Netherlands can provide more details on the types of services covered by these taxation rules.

VAT is also applicable to immovable property in the Netherlands. There are three cases when this tax applies, namely when an owner sells property, when he lets property or when he lets a holiday home. In the case of a sale, this applies when the purchaser is a private individual or a foreign entrepreneur or when the purchaser is an entrepreneur who is established in the Netherlands. V

AT is payable upon the same of a building or a part of a building with land within two years of its first occupation.

For letting immovable property, VAT applies for letting hotels, guesthouses, campsites, parking lots, mooring and storage places for vessels and in other situations. Homeowners who are frequently letting their holiday homes may be treated as an entrepreneur for VAT purposes, in case this happens frequently. When the holiday home is only purchased for private use, the tax is not applicable, however, whenever the home is let to guests directly or through intermediaries, the activity will be charged.

One of our attorneys in the Netherlands can provide more details about the situations in which VAT is applicable for selling or letting immovable property as well as for the use of a holiday home. In most cases, however, these activities related to the property are exempted from VAT.

If you want to open a company in the Netherlands and need assistance with the incorporation procedure, we can assist with it. We can also help with VAT registration in Netherlands.

Calculating the VAT in the Netherlands

Once the VAT registration is completed, the computation of the tax must be made in accordance with the requirements imposed by the Tax and Customs Administration in the Netherlands. The VAT is calculated based on the total amount of money charged on the customer which must include the value of the products, the delivery, the packaging and other costs. It is important to note that the depositing of goods is exempt from the VAT in the Netherlands.

Special attention must be paid upon the charge of the VAT for imports from EU and non-EU countries. Given the fact that the Netherlands is an EU member state, the EU intra-Community acquisition regulations apply, case in which the VAT will be charged in accordance with the VAT imposed by the supplier. When the amount of money is not in euros, it must be exchanged.

When importing goods from a non-EU country, the VAT will be calculated by the Dutch Customs Administration. If the amount of money on the invoice is not in euros, the amount will be converted into euros on the import declaration.

What are the VAT reporting requirements?

VAT registration in Netherlands is mandatory, however, the obligations of the entrepreneur do not stop with this step. They are also required to file VAT returns and pay the applicable VAT rates according to the law in force and by observing the terms.

VAT returns are filed on a monthly, quarterly, or annual basis, depending on the amount of VAT that is to be paid. When the VAT return is filed for the first time, the applicant is required to enclose all of the original invoices.

The Dutch authorities have the right to inspect the tax return and may ask for additional documents, such as copies of the issued invoices or the import documents, in addition to the original invoices for purchases that are usually required.

If you wish to open a company in the Netherlands in 2024 and need more details on the VAT requirements, please feel free to reach out to our team of tax lawyers. We can provide assistance for VAT registration once the company registration is complete as well as ongoing reporting assistance so that you can rest assured that your company complies with the requirements for VAT reporting. We can also provide investors with details on the Tax Plan package issued by the Government.

Additional information for the use of the VAT number in the Netherlands

VAT deregistration in the Netherlands is closely linked to the company’s registration status with the Chamber of Commerce (KVK). When the company is deregistered from the Chamber, it will also be deregistered from the Tax and Customs Administration. This is an automatic process that will lead to the termination of the VAT number. The process is to be notified to the entrepreneur via a written confirmation.

Investors should know that all companies in the Netherlands are required to use the new VAT identification number starting in January 2020.

The new number was introduced in order to offer a greater level of protection for entrepreneurs who are doing business in the country. The usage of the new number is important for the VAT returns issued starting with this date. Moreover, any requests for cross-border VAT refunds are to be issued by using the new VAT number in the Netherlands in 2020. New VAT identification numbers can be verified online, using the VIES platform. One of our lawyers can provide more details.

We also remind investors that EORI registration in Netherlands is required for the purpose of engaging in trading activities in and outside of the EU in 2024.

Company formation in the Netherlands is attractive for many entrepreneurs because of not only the favorable business regime and incentives for companies but also because of the country’s favorable location within the EU. According to Statistics Netherlands, the following numbers were recorded in regard to the investment climate in the country:

- 5.65% growth: the volume of investments in tangible fixed assets grew in October 2019 compared to the same month in 2018.

- 2.9: the indicator of the manufacturer’s confidence in December was up from 2.8 in November 2019.

- 119 bn EUR: the value of the domestic goods exports and 99 bn EUR service exports from the Netherlands 2017.

The data for 2023 in several areas is promising and shows further growth, according to data from the same source, Statistics Netherlands:

- the total volume of exported goods grew by 4.8% in January 2023, compared to the same month in 2022; the main increase was in the export of petroleum products, along with machinery and appliances; moreover, there is reason to believe that this trend will continue, with favorable circumstances expected for exports in March (according to the Exports Radar, CBS);

- the retail sector was also one to grow, reporting an 8.5% increase in February 2023, on a year-on-year basis; online retail increased by 6 percent and that in the non-food sector by 5.3%, year-on-year.

Reports from Statistics Netherlands on the economic situation throughout 2023 indicate that investments in tangible fixed assets grew in October 2023, on a year-on-year basis. Investments were higher in buildings and infrastructure, along with passenger cars, and fewer in computers. The data for December 2023 shows that consumer confidence increased between October and December.

As far as Dutch exports are concerned, a comprehensive evaluation from Statistics Netherlands shows that the volume of exported goods increased by 5.8% in the first quarter of 2023, and that of imports by 4.7%. The import volume in Q1 2023 was 3.9% higher compared to the same period a year prior.

Contact our Dutch law firm for further information and specialized support for VAT registration in Netherlands. We are able to provide you with a wide range of services on fiscal and legal support.

We can also help you with matters concerning private clients as we offer complete assistance during divorce in Netherlands.