When establishing a company in the Netherlands, investors may choose between setting up a subsidiary or a branch. The differences between these two business forms are substantial and our team of lawyers who specialize in opening branches and subsidiaries in the Netherlands can help you determine which one suits your business needs.

| Quick Facts | |

|---|---|

| Branches in Netherlands – definition |

Branches are permanent establishments established by foreign companies within the country in order to conduct their business activities without creating a separate legal entity; The branch is considered an extension of the foreign company. |

|

Subsidiaries in Netherlands – definition |

Subsidiaries are separate legal entities, owned and controlled by the parent company with their own legal status, assets, liabilities, and operations. |

|

Taxation of branches and subsidiaries |

– corporate income tax (19% on the initial EUR 200,000 of profit and 25.8% on any amount above that), – dividend withholding tax (15%), – withholding tax rate for interest and royalties (0%), etc. |

| VAT |

– 21% (standard rate), – 9% (reduced rate for food, medicine, etc.), – 0% (goods exported from EU); Please contact our team if you are interested in VAT registration in Netherlands. |

| Liability of branches |

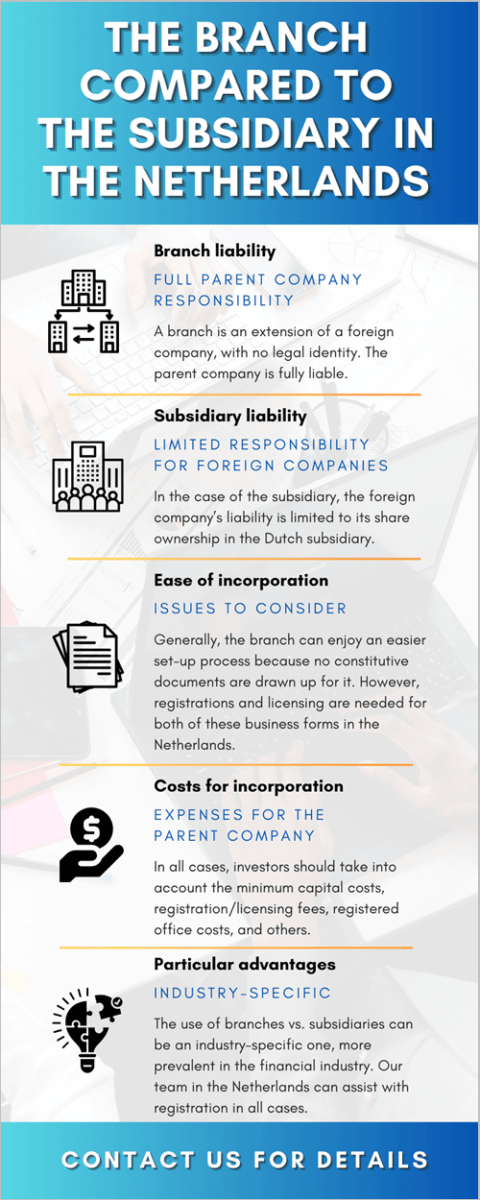

The parent company is responsible for all the debts and responsibilities of the Dutch branch. |

| Liability of subsidiaries |

The liability of a subsidiary is generally limited to its own assets and operations; The shareholders are only financially responsible for the amount of money they invested in the company’s capital. |

| Incorporation of branches |

Opening a branch involves presenting the foreign company’s existing Articles of Incorporation and the decision to establish the Dutch branch, and registering with the Trade Registry and Chamber of Commerce; Our Dutch lawyers can help. |

| Incorporation of subsidiaries |

Opening a subsidiary involves drafting new Articles of Association; Registration with the Trade Registry and Chamber of Commerce is still mandatory. |

| Double taxation agreements |

Subsidiaries have access to double taxation treaties, unlike branches, with a few exceptions. |

| Accounting | Both branches and subsidiaries are required to comply with Dutch reporting and tax regulations, but the accounting practice and financial reporting is different. |

| Recommended for |

Companies looking for a simple entry into a new market (branches); Businesses seeking external investments or partnerships (subsidiaries). |

| Capital requirements |

– 0.01 EUR (if the legal entity is BV for a subsidiary), – no minimum capital (branch). |

| Advantages of opening a branch in Netherlands |

– easy incorporation process, – the branches’ financial statements do not need to be published, – no minimum share capital required, – a great opportunity to enter a new market. |

| Advantages of opening a subsidiary in Netherlands |

– limited liability of the shareholders, – the parent company is not liable for the subsidiary, – customers and partners might have more trust in a local brand, – intangible assets can be amortized for Dutch tax purposes. |

| Assistance | If you have trouble choosing between opening a subsidiary or branch, our law firm can help. |

Different circumstances and the company’s interests may ultimately determine the choice between the two legal entities, but certain aspects need to be taken into consideration when making a choice between a branch and a subsidiary in the Netherlands.

We recommend that foreign companies interested in exploring their options reach out to our experienced lawyers. We are a multi-service law firm in the Netherlands, focusing its activities on providing reliable legal solutions for businesses. We can advise our foreign clients from the earliest stages of their expansion project, by providing reliable information on the differences, and the advantages of the Dutch branch and the Dutch subsidiary.

If you would like to know more than the descriptions and the differences presented herein, please reach out to our team for personalized information on how to open a subsidiary in the Netherlands or a branch.

Table of Contents

Branches in the Netherlands

A branch is a permanent establishment that forms one entity with a foreign company. It is essentially an extension of the parent company abroad and thus the parent company will need to undertake the liabilities that arise from opening a Dutch branch. This particularity offers both advantages and disadvantages.

Foreign investors willing to establish a branch in the Netherlands can read the list below which summarizes the main characteristics of this business form:

- set up advantages: it is relatively easy to set up and the costs are usually lower compared to incorporating a new legal entity.

- slightly different taxation regime: no withholding tax on remitted earnings and no capital registration tax; the loss of the Dutch branch may be offset against taxes/profits of the head office; the problem of double taxation may arise in the case of a permanent establishment.

- different accounting principles: no need to publish the financial result of the branch (with some exceptions).

- no legal capacity: the branch is not a separate Dutch legal entity, it operates as a foreign company.

- liability: the parent company that will set up a branch in the Netherlands will be fully liable for the debts and obligations of the Dutch branch; also, acceptance may be harder to gain from Dutch nationals because of the foreign identity of the branch.

Below, we further talk about the main characteristics of branches and subsidiaries in the Netherlands.

The branch is generally perceived as a business form that has lighter incorporation and management requirements compared to the subsidiary. The registration with the Trade Registry is still needed for the branch, however, the process is simpler because the foreign company will present its already existing Articles of Incorporation and the decision to set up the Dutch branch. As a comparison, for the subsidiary, the Articles of Association will need to be drafted as new documents. Registration with the Chamber of Commerce will also be needed for the branch.

The documents usually needed to open a branch in the Netherlands in 2024 include the following: the parent company’s constitutive documents such as the Memorandum and Articles of Association, its registration certificate issued by the country of residence, the names and identification documents of its directors, the name and identification documents for the branch representative in the Netherlands (as well as a description of its powers and duties), the decision to establish the branch and details regarding its address and name.

After it is registered with the Company Register, the branch will also need to be registered for tax purposes and for social security purposes as it will hire employees. In terms of taxation, the branch is taxed at the same corporate income tax rate of 19% on the first 200,000 EUR of taxable profits and 25.8% over this amount. In some cases, the branch may qualify as a permanent establishment in the Netherlands, however, the principle of taxation for a branch is solely on its Dutch-derived profits. One of our Dutch lawyers who specialize in branch and subsidiary creation can help you with detailed information about taxation.

The representative office is another manner in which a foreign company can establish its presence in the Dutch market, however, it is more limited compared to the branch. It can only engage in marketing or promotional activities and cannot derive profits – therefore no registration with the tax authorities is needed.

Typically, a representative or liaison office is only used in limited cases, such as for testing the Dutch market, keeping in contact with local clients, customers, and, in some cases, suppliers or business partners, or for other activities that may promote or engage the foreign company abroad, creating a favorable image for this foreign company in the Netherlands. Because this business form is only used in some cases, our team of attorneys in the Netherlands can give you more details.

Subsidiaries in the Netherlands in 2024

For companies that establish a subsidiary in the Netherlands, the main advantage is the shareholder’s limited liability but other aspects need to be taken into consideration. The main advantages and disadvantages are highlighted in the following list:

Subsidiary advantages:

- the shareholders have limited liability, to the extent of their contribution to the capital;

- unless agreed otherwise, the parent company is not liable for the Dutch subsidiary;

- intangible assets can be amortized for Dutch tax purposes;

- Dutch nationals may prefer dealing with a subsidiary;

Subsidiary disadvantages:

- more complicated to set up and more expensive;

- withholding tax on remitted earnings;

- medium and large companies must publish their financial statements;

- the appointment of at least one director is required by law.

The set up of a subsidiary in the Netherlands is perceived as a more complex process compared to the establishment of a branch because although the final registration steps will need to be handled just the same, it is incorporated through a notarial deed and the founders will also need to draw up the Memorandum and Articles of Association.

One of our lawyers in the Netherlands can help you draw up the company documents according to the chosen business type. In most cases, this will be the private limited liability company or the BV because it offers advantages both in terms of investor liability (the founders are only liable to the extent of the capital they invest) and also because it has very low requirements for the start-up capital. Public limited liability companies can also be used as subsidiaries in the Netherlands. These will require a substantially larger initial share capital and will also have different accounting and auditing requirements as their shares can be publicly traded.

Foreign investors should consider this list of primary advantages and disadvantages when deciding between a subsidiary and a branch in the Netherlands. Scheduling a consultation with our team of lawyers who specialize in opening branches and subsidiaries in Netherlands can help foreign investors decide which business form will be suited to their business needs. It is advisable to work with our team of lawyers before establishing a legal entity in the Netherlands in order to fully understand the taxation, accounting, and reporting principles as well as liability for each business form.

When a subsidiary engages in trade activities within the EU, it is subject to EORI registration in Netherlands.

In the Netherlands, the subsidiary tends to be a preferred business form in many fields, although in sectors like banking and finance, large international companies will open branches. The subsidiary is able to engage in more than one type of business activity and the fact that it is not limited to one business purpose, the same as its parent company abroad, can be advantageous for some types of business activities. It is useful to know that VAT registration in Netherlands may be required for a subsidiary.

Additionally, the subsidiary will be a locally registered company in which the foreign entity will hold a percentage of shares (and thus control it). It will need to apply for special permits and licenses when operating in some business fields. Companies in the manufacturing business, the hospitality sector, the pharmaceutical sector, and many other industries need to obtain licenses and/or approvals from the relevant Dutch authorities. Our lawyers can give you details on specific licenses and assist you throughout the application process.

The video below describes the main differences between the two business forms:

Branch and subsidiary taxation and reporting in the Netherlands

The branch and the subsidiary are subject to the same corporate income tax rate in the Netherlands, however, the basis for residence is different, as it depends on where the company has its management office. Our team of lawyers in the Netherlands can provide a complete definition of residence, however, the principle is that resident companies (such as subsidiaries, that have their management in the country) are taxed on their worldwide income while nonresident companies (such as the branch, which is dependent on the parent company abroad) are taxed only on the income sourced from the Netherlands.

Below, we highlight some of the most important taxes:

- 19%: the corporate income tax on the first 200,000 EUR of taxable profits;

- 25.8%: the applicable corporate income tax rate on taxable profits that exceed 200,000 EUR;

- 15%: the dividend withholding tax rate, unless reduced or exempted through a tax treaty or the EU parent-subsidiary directive;

- 0%: the withholding tax rate for interest and royalties applicable both to residents and nonresident companies;

- 21%: the standard value-added tax in the Netherlands, along with two reduced rates of 0% and 9% that apply to certain types of foods and services (foodstuffs, medicines, books, or goods that are exported from the EU).

Adjustments have been made to the job-related investment credit and there is the introduction of a unilateral air passenger tax (to be levied from airport operators). We can provide more information on the Tax Plan Package upon request.

Our team of tax lawyers in the Netherlands can provide complete information on the tax requirements for branches and subsidiaries – which, as seen above, are similar in many aspects. We can offer information on the EU parent-subsidiary directive and we can guide entrepreneurs during the VAT registration process (this is mandatory for companies that provide certain goods and services as there is no registration threshold, all VAT payers must register).

Social security contributions are mandatory both on the part of the employer and the employee and companies are required to withhold tax on the wages paid to their employees. A particularity of the payroll tax in the Netherlands applies in the case of foreign employees in the form of a 30% deduction for a period of five years (during this time, a tax-free allowance of 30% of the gross remuneration for these employees is applicable and our lawyers can detail the advantages of hiring foreign employees for a branch or a subsidiary).

As far as accounting and reporting are concerned, the tax year in the Netherlands is generally the same as the calendar year and the accounting principles that apply are the Dutch GAAP, with the possibility to also use the International Accounting Standards and the International Financial Reporting Standards.

Consolidated returns are possible in the case of parent companies. This means that, under certain conditions, these companies may be treated as having fiscal unity with one or more subsidiaries, according to which the losses of one company can be offset against the profits of another. For this to be possible, the parent company needs to own at least 95% of the economic and legal ownership of shares of the subsidiary. Moreover, the parent company and the subsidiary in the Netherlands need to have the same financial year. It is possible in some cases for the Dutch permanent establishment of a foreign company to be included for this purpose (be included as a fiscal unity).

Companies in the Netherlands are expected to file a provisional assessment, which is commonly based on information from the previous two years. Monthly installments are used to pay this assessment for the remainder of the year. Corporate income tax returns are filed each year within five months of the end of the tax year – in some cases, an extension is possible.

When filing the corporate income tax return, the company also provides relevant documents such as the balance sheet and the profits and loss account. Administrative penalties apply in case of late filing or incomplete filing. Criminal penalties are also possible if the Dutch authorities prove gross negligence or fraud. Our litigation attorneys in the Netherlands can provide more details.

Foreign investments in the Netherlands

According to the European Central Bank, Statistical Data Warehouse, there were 1,076 branches of credit institutions providing cash services in the Netherlands in the first half of 2020. Their number was higher in the first half of 2019, at 1,305.

Statistics Netherlands also offers relevant data on foreign direct investment in the country. To highlight some of the trends, our team compiles a set of data to reveal the top investors in the Netherlands:

- the investment volume grew by 3.3 percent in July 2023, on a year-on-year basis;

- the most significant investment percentages were recorded in the fields of transport equipment and buildings, with the first including those in passenger cars, but also other road transportation means and aircraft;

- also in July 2023, the volume of imported goods was 2.2% higher when compared to the same month a year prior.

Statistics Netherlands also offers us a glimpse into the volume of investments in tangible assets:

- in October 2023, investments in tangible assets rose by 2.5% compared to the same period a year prior;

- most of the investments took place in infrastructure, business, and passenger cars; by comparison, investments in computers accounted for less of these types of investments.

In addition to the data concerning tangible assets investments, Statistics Netherlands also evaluates the manufacturer’s confidence levels and reports show that this is improving in January 2024. Overall, manufacturers were more positive about the expected output for the following three months. Producers in the electrotechnical and machinery industries were most confident.

Doing business in the Netherlands

The branch can be a convenient manner to enter the Dutch market for foreign companies in the financial sector. In other cases, the Dutch branch can act as a first step, before incorporating a BV or an NV. The faster establishment process can be an advantage for foreign investors, especially in the early stages of doing business in the Netherlands.

Regardless of the business form incorporated in the country, having reliable legal assistance from a local team of attorneys such as our own is helpful for remaining compliant with the current requirements. We advise foreign investors (both natural and legal persons) on the most suitable business form they may choose for entering the Dutch market but are also able to answer important questions about taxation, or remaining in the country lawfully for longer periods, in the case of non-EU investors who plan on residing in the Netherlands.

Our team can also help you with the post-registration steps for doing business in the Netherlands. This refers not only to obtaining the needed special permits and licenses for functioning but also to hiring employees. Both branches and subsidiaries need to follow the rules for hiring staff and the assistance of an employment lawyer, such as one from our team, is helpful both during pre-employment and after the employment has taken place.

It is not uncommon for branches or subsidiaries of foreign companies to hire foreign staff, or even perform cross-border employee transfers. As a general rule, the employer will be first asked to try and hire staff from the EEA area and/or Switzerland. If this is not possible (by providing sufficient proof), then the company will be allowed to recruit from other countries. If this becomes the case, the company will need to take the needed steps to apply for a Single Permit for the respective non-EEA employee (this is a work permit and a residence permit combined).

The employer is also required to provide the foreign staff with suitable accommodation for those who will work at the branch or subsidiary. If this is the case, the rules may differ according to municipality, and we recommend discussing the requirements with our local lawyers.

Outsourcing work, hiring foreign or local staff, as well as handling various other matters once the registration of the branch or the subsidiary is finalized are all important steps. Our team is ready to answer any questions about the current business and trade laws, relevant employment provisions, as well as issues concerning agreements and contracts, before or after you complete the registration of the Dutch subsidiary or branch.

If you need more information or need help deciding what type of company is best to establish in the Netherlands in 2024, please contact our lawyers who specialize in opening branches and subsidiaries in the Netherlands.